Flagstar Mortgages May Be A Savior As NYCB Shores Up Steadiness Sheet

Mark your calendars for the final word actual property experiences with Inman’s upcoming occasions! Dive into the longer term at Join Miami, immerse in luxurious at Luxurious Join, and converge with trade leaders at Inman Join Las Vegas. Uncover extra and be part of the trade’s finest at inman.com/events.

Plummeting industrial actual property values might immediate New York Neighborhood Bancorp to faucet a extra steady asset to shore up its stability sheet: residential mortgages originated when rates of interest have been low.

New York Neighborhood Bancorp (NYCB) is seeking to pledge about $5 billion in residence loans originated by Flagstar Financial institution as backing for a “artificial danger switch” that may bolster its capital reserves, Bloomberg reported Wednesday, citing nameless sources with data of the talks.

NYCB, which acquired Flagstar Bank 2022, is one among various regional lenders that would want recent capital if the efficiency of loans they made to industrial builders continues to deteriorate. With workplace and retail vacancies remaining elevated in lots of markets after the pandemic, the properties that served as collateral for the loans are, in some instances, price lower than the excellent stability on loans.

Since reporting a $252 million fourth-quarter loss on Jan. 31, NYCB shares have misplaced greater than half their worth. Shares within the financial institution, which hit a 52-week high of $14.22 on July 28, briefly touched a 52-week low of $3.60 Wednesday earlier than climbing again above $4.

In reporting earnings, NYCB stated it boosted its provision for credit score losses by 533 %, to $833 million. Fourth quarter charge-offs of $117 million in multifamily and $42 million in industrial actual property loans additionally sounded alarm bells with buyers. These issues have been amplified when Fitch Ratings and Moody’s Traders Service downgraded NYCB’s credit score scores, which may make it extra pricey for the financial institution to borrow cash.

“When it comes to monetary technique, the financial institution is in search of to construct its capital however simply took an unanticipated loss on industrial actual property which is a big focus for the financial institution,” Moody’s analysts said Tuesday.

Moody’s analysts stated they have been additionally involved in regards to the departure of NYCB’s chief danger officer, Nick Munson, and chief audit officer, Meagan Belfinger, who left the corporate unannounced earlier than earnings have been launched.

After the scores downgrade, NYCB announced Wednesday that it was appointing former Flagstar Financial institution President and CEO Sandro DiNello as govt chairman. DiNello, who was previously non-executive chairman, will “work alongside” the chief who spearheaded the Flagstar merger, NYCB President and CEO Thomas Cangemi, “to enhance all facets of the financial institution’s operations.”

Cangemi introduced Wednesday that NYCB is within the technique of bringing in a brand new chief danger officer and chief audit govt with massive financial institution expertise, “and we at present have certified personnel filling these positions on an interim foundation.”

In an try to reassure buyers and purchasers, NYCB also publicized that its deposits have continued to develop this yr, to $83 billion, and that its $37.3 billion in whole liquidity exceeds uninsured deposits of $22.9 billion.

Whereas NYCB’s share value has stabilized, Morningstar DBRS joined Fitch and Moody’s in downgrading the financial institution’s credit score scores Thursday.

“At $37.3 billion, liquidity seems ample, however given the financial institution failures final spring, we stay cautious provided that the antagonistic headline danger, together with a big decline in NYCB’s inventory value, may ultimately spook buyer and depositor confidence,” Morningstar DBRS analysts said.

Final yr’s failures of Silicon Valley Financial institution, Signature Financial institution and First Republic Financial institution — largely pushed by rising rates of interest — put regional banks below heightened scrutiny by scores businesses.

NYCB claims to be the second-largest multifamily residential portfolio lender within the nation, and the main multifamily lender within the New York Metropolis market space, specializing in rent-regulated, non-luxury condominium buildings.

“NYCB’s core historic industrial actual property lending, vital and unanticipated loss on its New York workplace and multifamily property may create potential confidence sensitivity,” Moody’s analysts stated in downgrading NYCB’s credit score scores to junk standing. “The corporate’s elevated use of market funding might restrict the financial institution’s monetary flexibility within the present surroundings.”

Former FDIC Chair Sheila Bair told Yahoo Finance Thursday that the majority multifamily housing — which is included within the industrial actual property class — is definitely “ place to be. However in sure pockets, notably in New York, the place we have now some fairly restrictive lease management legal guidelines, you’re seeing some misery.”

Bair stated that whereas it’s essential to not “taint your entire sector,” there are issues in segments of CRE together with city workplace and a few city retail. Many regional banks “do have heavy publicity to distressed components of the market they usually’re gonna have to work by that.”

“Hopefully, they reserved sufficient,” Bair stated. “However we’ll see. In the event that they don’t, we’re gonna have most likely a number of extra financial institution failures. Nevertheless it’s nothing like what we noticed throughout 2008.”

Showing on 60 Minutes Sunday, Federal Reserve Chair Jerome Powell said that whereas he doesn’t anticipate a repeat of the 2008 monetary disaster, “there will probably be some banks that must be closed or merged out of existence due to this. That’ll be smaller banks, I believe, for essentially the most half.”

The newest worries over industrial actual property values may make jumbo mortgages costlier and more durable to come back by, since regional banks have historically been a number one supplier.

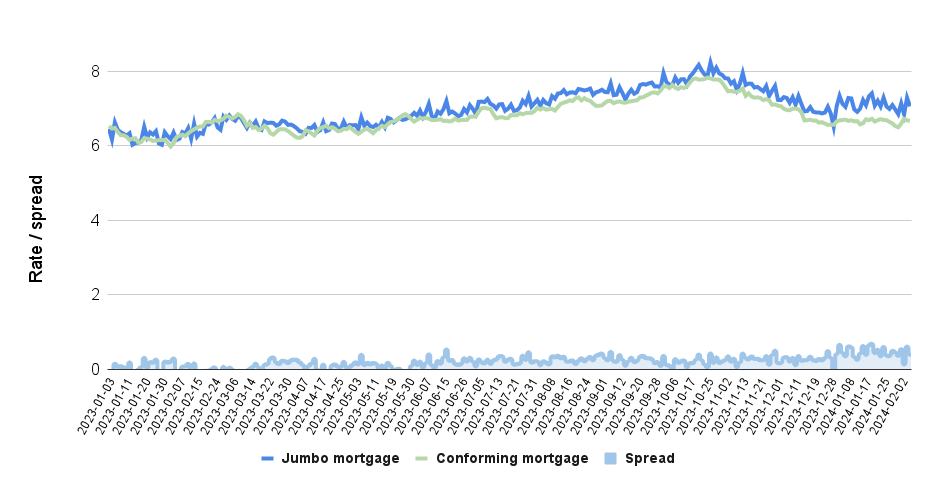

In line with every day fee lock knowledge tracked by the Optimal Blue Mortgage Market Indices, the “unfold” between charges for jumbo and conforming mortgages widened after the March 10, 2023 closure of Silicon Valley Financial institution — a pattern that’s continued this yr.

Widening conforming, jumbo mortgage ‘unfold’

Historic unfold between charges on jumbo and conforming mortgages. Supply: Inman evaluation of Optimum Blue fee lock knowledge retrieved from FRED, Federal Reserve Financial institution of St. Louis.

“In contrast to conforming loans, that are largely financed by mortgage-backed securities (MBS) by way of capital markets, the jumbo mortgage area is nearly solely funded by way of the banking sector, and a few regional banks are extra concentrated in jumbo mortgage lending than others,” Fannie Mae forecasters warned final March. “Ongoing liquidity stress may restrict residence financing and due to this fact gross sales within the associated market segments and geographies with excessive jumbo focus.”

Throughout January and February of 2023, Optimum Blue knowledge reveals the unfold between jumbo and conforming mortgages averaged about 1 foundation level, with charges on jumbo mortgages at occasions decrease than charges for conforming mortgages (a foundation level is one hundredth of a share level).

Through the remaining 10 months of 2023, from March by December, the unfold averaged 19 foundation factors. To this point this yr, by Feb. 7, the unfold has averaged 46 foundation factors — practically half a share level.

Get Inman’s Mortgage Brief Newsletter delivered proper to your inbox. A weekly roundup of all the largest information on this planet of mortgages and closings delivered each Wednesday. Click here to subscribe.